office (412)

9679367

office (412)

96793672.5 A Tour of the Form 10-K: The Structure

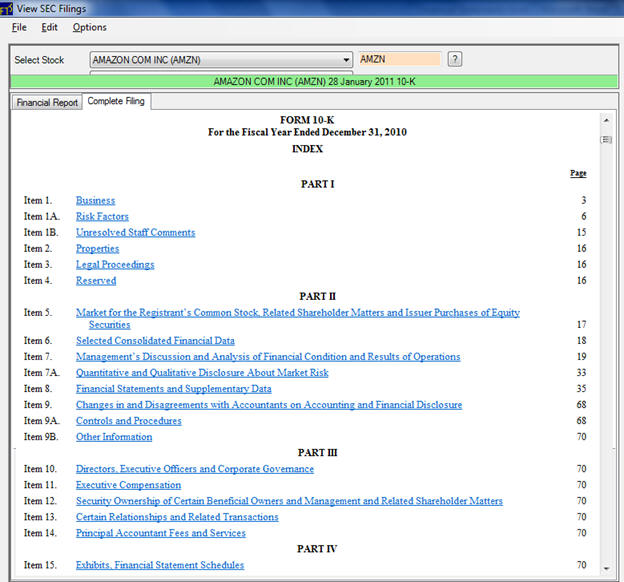

The following figure shows

a sample of the 10-K items as reported by Amazon.com.

We will highlight some of the important Items from an

accounting and financial analyst perspective. The structure is

mandated by the SEC for publicly held corporations.

As a result, the same format applies to any public

corporation:

From the point of view of

Financial Statement Analysis and Valuation, the following items are

important:

·

Item 1 describes the

business model and strategy.

We described these in the introduction, and will return to

this in Chapter 3.

o

Item 1A identifies all the

major risks faced by the company.

Unfortunately, it does not indicate the likelihood of the

risks but it does provide an exhaustive list, given potential

regulatory penalties faced by management today.

·

Item 7 contains information

that cannot be found in the financial statements.

This item is intended to cover favorable and unfavorable

trends or events relating to liquidity, capital expenditures,

financing and operations.

We will give examples of this below

·

Item 8 contains the four

major statements: the income statement, the balance sheet, the

statement of shareholder’s equity, and the cash flow statement.

We describe these in detail in the next few sections of this

chapter.

·

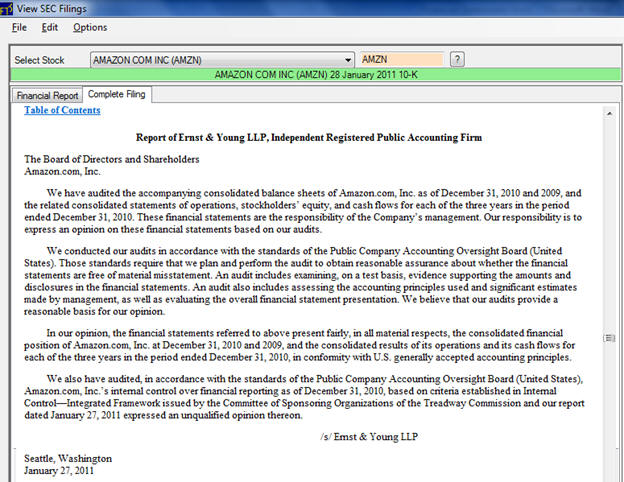

Item 9 contains the

Auditor’s Report. This

is a statement from the independent auditors on whether or not the

financial statements “present fairly, in all material respects, the

financial position” of the company.

o

An

unqualified report states that the major financial statements are

fairly presented in all material respects and are in compliance with

GAAP.

o

A

qualified report which

uses the language that except for certain items, the report is

unqualified.

o

An

adverse opinion is given if departures from GAAP are numerous.

o

A

disclaimer of opinion can be issued which effectively means the

auditor is unable to form an opinion.

o

An example of an auditor’s

report is: