A.1

Appendix:

A Quick Tour of the Balance Sheet

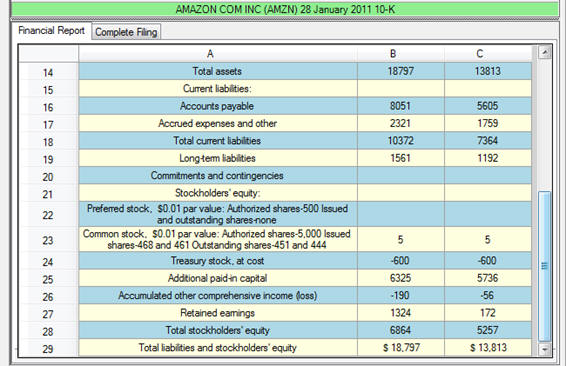

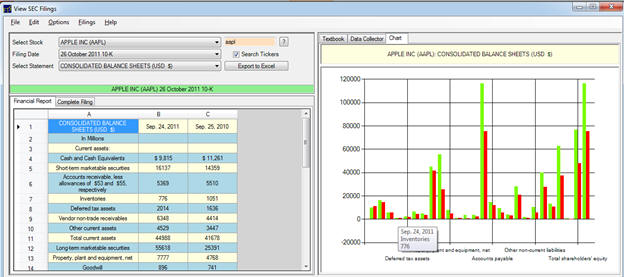

A.1: Consolidated

Balance Sheet (Example: Amazon, Jan 2011 10-K)

This statement provides the primary source of information relevant

to assessing the capital resources that a company controls.

It shows the financial position -- assets, liabilities and

stockholders' equity on a particular date.

The formal structure of the Balance sheet at a point in time

is:

Assets - Liabilities = Owners Equity

That is what resources are available less what obligations the

entity has equals the owners’ residual claims.

That is, if you purchased this entity the balance sheet

provides the set of resources you gain control over plus the set of

obligations or liabilities that you have assumed.

The balance sheet results from classifying every transactions

relative to the fundamental accounting equation.

That is, the balance sheet results from the following types

of transactions:

o

Assets increase, Assets decrease

o

Assets increase, Equities increase

o

Equities decrease, Equities increase

o

Equities decrease, Assets decrease

o

Assets and equities increase or decrease by the same amount

In each case the equality is maintained.

For example suppose Wal-Mart purchase inventory for cash to

sell in their stores.

Inventory is an asset and so assets increase.

Cash is an asset that is decreased and thus the net effect is

unchanged leaving the fundamental equation unchanged.

Other transactions may result in increasing the two sides of

the above equation by the same amount.

For example, suppose Wal-Mart sell this inventory for cash at

a higher price than what they paid for it.

Now the cash asset increases more than the inventory asset

decreases which requires for equality to be restored by adding the

difference (referred to as the profit) to the right hand side of the

equation in retained earnings an owners’ equity account.

One could ask do any transactions exist that only have a single

effect?

The answer is no because

the accounting equation is a binding constraint and therefore the

accounting equation identifies the appropriate offset for

every transaction.

In other words double entry accounting flows naturally from

the accounting equation that defines the balance sheet.

For example, paying a cash dividend may appear to fall into a

possible single effect category because cash is paid out.

So what is the offsetting entry?

The answer to this is that because cash is paid out to the

owners this reduces owners’ equity and thus cash dividends reduce

assets and reduce owners’ equity (retained earnings).

Balance Sheet Classifications and Major Firm Decisions

In the balance sheet assets provide future services to the firm.

They are classified into Current and Non-Current Assets if

their service potential is short term (either 1-year or one

operating cycle if the latter is greater than 1-year).

The Operating cycle is defined as the time to purchase or

manufacture inventory, sell the product and collect the cash.

The operating cycle is short for the case of perishables

such as food, seafood, fruit and relatively short in consumer goods

industries. It is

slower in capital goods industries and relatively long for products

such as distilleries and wine.

As a result, in these industries the one operating period

rule sometimes applies.

Non-current assets reflect investments the firm has made into capacity and related items so that their service potential to the firm extends over longer periods of time. Similarly, Liabilities are classified into Current and Non-Current based upon the time of the obligation’s expected due date. Obligations can arise from operations such as accounts payable, from investing activities and financing activities the entity is involved in. Finally, the owners or stockholders’ equity part of the balance sheet results from transactions involving shareholders such as new equity financing or company purchases of their own stock (Treasury stock purchases) as well as activities not involving shareholders but the shareholders benefit from. For example, income generating activities, foreign currency fluctuations, pension accounting and fair value accounting. An example is provided below for Amazon.com.

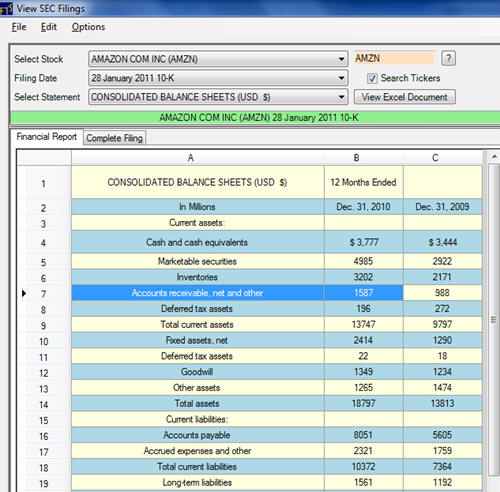

Amazon present their balance sheet in a relatively simple form

compared to most other companies.

They provide their additional details in separate support

statements. For

example, suppose an analyst wanted to see what the above reported

number for “Long Term Liabilities” $1561 (millions) consist of?

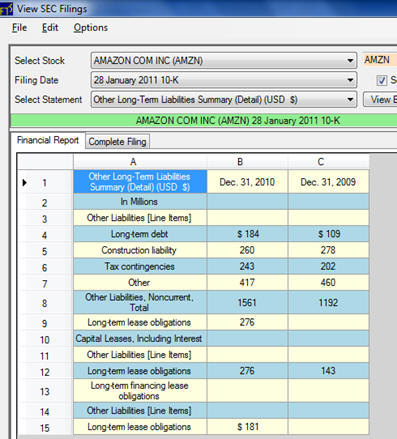

For Amazon this is in the support statement (“Other Long-Term Liabilities Summary (Detail) (USD $)”):

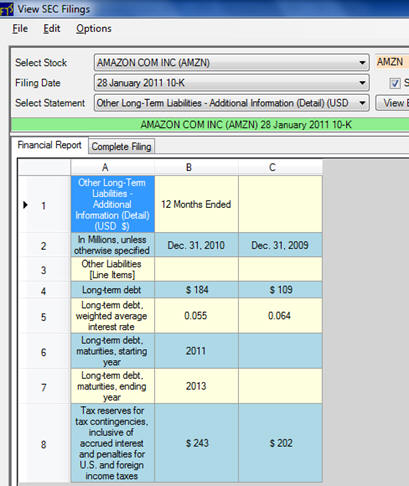

Further details are available about Amazon’s Long Term Debt including the weighted-average interest rate as follows:

Online, you can also drill down into Amazon’s lease obligations by

selecting the statement “Long-Term Capital Lease Obligations

(Detail) (USD $)”:

The Stockholders Equity is provided below to preserve links between

the two balance sheets across time.

In a separate topic we will work through the details of the

stockholders’ equity section of the balance sheet.

This is because this area is sufficiently complex that today

it is expanded into the fourth primary statement referred to as the

“Consolidated Statement of Stockholders’ Equity.”

Next, we consider some of the typical line items in a Consolidated

Balance sheet.

Elements of the Balance sheet

Current Assets

US GAAP requires listing in order of liquidity and it includes the

following major categories:

Cash and Marketable Securities (Category:

Cash)

Cash and cash substitutes, relatively riskless and easily converted

to cash. Marketable

securities are short term investments that are initially recorded at

cost. However, US GAAP

(FAS 115) categorizes marketable securities into three categories;

Trading, Available for Sale, Held to Maturity.

To categorize as “Held to Maturity” the firm must have

‘positive intent and ability’ to hold until maturity.

Marketable securities held for trading are common for

financial institutions.

In addition, for all institutions there are some financial

securities that are deemed to be Held-for-Trading irrespective of

intent. These are

derivatives that do not qualify as a hedge under US GAAP.

Finally, any security that is neither classified as “Trading” or

“Held to Maturity,” are deemed to be “Available for Sale.”

The classification matters for how it is measured on the

balance sheet relative to recognizing unrealized gains and losses.

In particular,

•

Held to maturity

– These are measured on the balance sheet at amortized cost.

•

Trading securities

– These securities are reported at fair (market) value with

unrealized gains and losses reported in the accounting income

statement (covered in a later topic).

•

Available for Sale

– These securities are neither “Held-to-Maturity” or for “Trading.”

Available-for-Sale securities are reported at fair value with

unrealized gains and losses reported in the Consolidated Statement

of Stockholders’ Equity (covered in a later topic).

It is noted that accounting for financial assets reflects fair value

accounting and is one of those rare examples of where the

recognition of unrealized

gains is permitted.

Of course the recognition of unrealized losses is common in both

historical cost and fair value accounting.

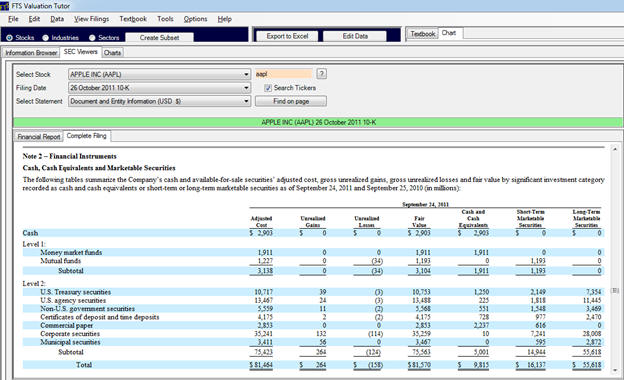

Financial assets on today’s balance sheet can be very large.

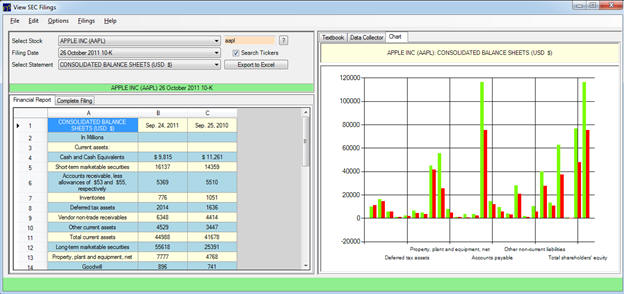

The example below illustrates this for Apple (in millions):

The breakdown of this category for large firms is provided in their

footnotes to the account:

The next set of account groupings fall into the category of working

capital. Working

Capital measures the operating liquidity of a firm and results from

managing a firm’s short term assets and liabilities that relate to

the firm’s operations.

Major items include:

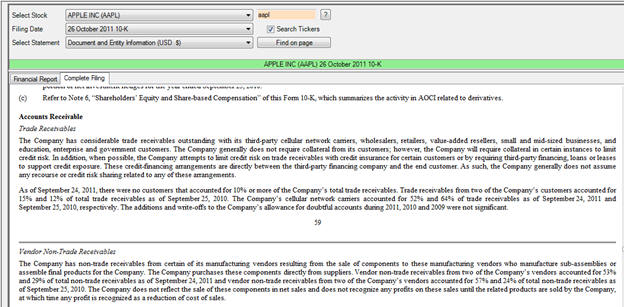

Accounts Receivable (Category:

Operating)

This records the outstanding balance from credit sales and is

recorded at their net realizable value.

That is, an allowance is made for doubtful debts.

Again important details associated with the Accounts Receivable are

provided in the footnotes to the accounts.

Inventory (Category:

Operating)

This records items that held for sale or used to manufacture

products to be sold.

The measurement of inventory reflects the underlying cost flow

assumption which under US GAAP can be FIFO (first-in, first-out),

LIFO (last in, last out), weighted average cost or specific

identification. Under

IFRS only FIFO the weighted average cost flow assumptions are

permitted. The cost

flow assumption for accounting purposes can be different from the

actual physical flow of inventory and in times of inflation the cost

flow assumption makes a significant difference to net income

measurement. That is,

LIFO reduces income but also reduces taxable income in times of

inflation relative to FIFO.

Analysts look at the change in inventory over the period to check

whether inventory is building up or running down.

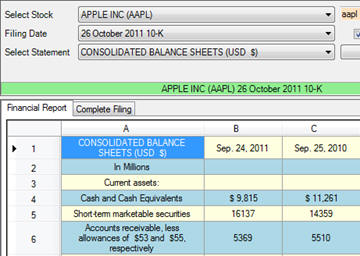

When product is moving fast inventory declines as can be seen

from Apple’s results below:

Prepaid Expenses (Category:

Operating)

Not all current assets are converted to cash.

Prepaid expenses represent one class that does not convert to

cash but they do have service potential that will be consumed within

the year. Typically

these are insurance, rent, property taxes and utilities.

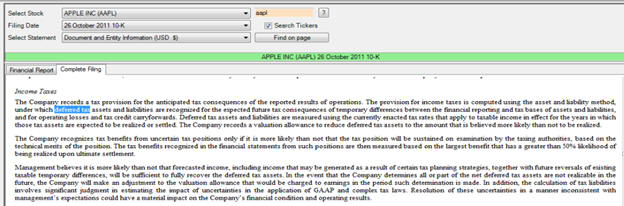

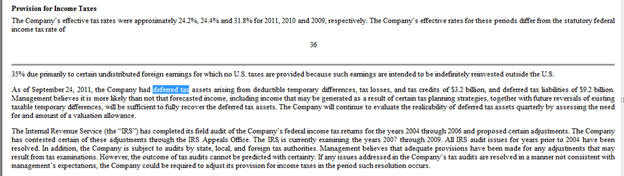

Deferred Taxes (Category:

Operating)

This item can appear as a current asset in a balance sheet.

It arises because accounting net income and taxable income

are different. For

example, in taxable income there can be effects from net loss

carryovers from previous periods which are classified as assets when

it is determined that there is a greater than 50% chance of being

able to be used in future fiscal periods.

As a result, differences

between accounting and taxable income can be classified as either

“temporary” or “permanent.”

Deferred taxes arise from

temporary differences in

the recognition for taxable income and this can create either an

asset or a liability on the balance sheet.

Deferred taxes in the “current” part of the balance sheet reconciles

the differences for the current accounting period between the

reported tax expense and the cash paid for taxes to the IRS.

Apple Example:

Again it is in the footnotes to the accounts that spell out the

differences as illustrated for Apple below.

Non-Current Assets

Property, Plant and Equipment (PPE) (Category:

Investing)

These items represent the firm’s capacity to provide service for

more than one year.

These items are depreciated over time and management has much

discretion with respect to their choice of depreciation methods.

Briefly the three major types are referred to as straight

line, accelerated and units of production.

Noncurrent assets are cleverly defined as anything not classified as

a current asset. The main line items in this section are long-term

investments; property, plant, and equipment (PP&E); and goodwill and

other intangible assets.

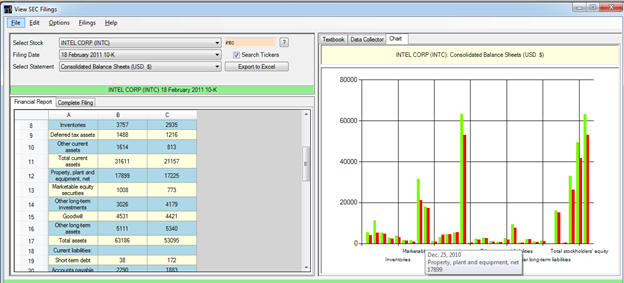

The relative size of PPE depends upon the firm’s business model and

it is instructive to illustrate this for Apple versus Intel.

Intel produces chips and there products whereas Apple focuses

upon interface and excels at interface with the human user.

Such differences will appear both in Item 1 of the 10-K as

well as their respective balance sheets:

Example: Apple versus

Intel

The graph reveals the relative small size of PPE to other Balance

Sheet items for Apple.

Now compare this to the large relative size of PPE for Intel.

This is consistent with its business model:

Leases (Category:

Investing)

Under both US GAAP and IFRS leases are recognized as an asset if the

firm bears substantially all the risks and rewards of ownership of

the leased property.

This is classified as a capital lease.

We will return to leases in more detail in the Liability side

of the Balance Sheet.

Deferred Taxes (Category:

Operating)

This item can appear as a non-current asset in a balance sheet.

It arises from net loss carryovers which are classified as

assets when it is determined that there is a greater than 50% chance

of being able to be used in future fiscal periods.

Refer to the discussion in

the Current section for additional information on this category.

Pensions (Category:

Operating)

Pension accounting will be discussed in more detail later in the

Consolidated Stockholders’ Equity topic.

Long-Term Investments

(Category: Investing)

These items represent investments that are expected to be held for

longer terms than one year. These items will include a number of

different measurement bases ranging from fair value to historical

costs. Additional

details are provided in the notes to the financial statements.

Intangible Assets (Category:

Investing)

These items represent nonmonetary assets without physical substance.

To be recognized on the Balance sheet there should be

probable future economic benefits and costs should be reliably

measured. Goodwill is

only recognized in a business combination and research costs

associated with Research and Development (R&D) are expensed for most

industries.

January 1, 2002 the Financial Accounting Standards Board (FASB)

eliminated the “pooling method” of accounting which meant that

goodwill and intangibles are no longer amortized.

Instead under fair value accounting they are placed on the

Balance Sheet but subjected to annual tests for impairment.

Impairment under US GAAP has a technical meaning.

It is the downward revaluation of a fixed asset below its

historical cost and impairment write downs cannot be subsequently

recovered via upward revaluation even if the asset has subsequently

recovered in value.

This is a major current difference between US GAAP and IFRS.

IFRS permits recovery of prior impairments (up to the

original historical cost) if the value has subsequently recovered.

It is noted that neither system allows unrealized gains to be

recognized unlike the earlier cases that involved financial assets.

A Classic Example of Accounting for Goodwill

The worst takeover in US Corporate History was the Time Warner/AOL

merger. At the time of

the merger, even though financial analysts made upbeat comments,

technology had changed and the merger made little sense given that

AOL’s user base relied entirely upon dial up web services.

Further, AOL had

no ability to provide

the new trends of delivery via cable and other high speed delivery

methods because other entities controlled these outlets. However, at

the time of the merger typical reporting was as illustrated below:

That’s AOL folks…

January

10, 2000: 5:26 p.m. ET

Internet leader and entertainment firm to

join forces; new company worth $350B

By Staff Writer Tom Johnson

NEW YORK (CNNfn) - In a stunning

development, America Online Inc. announced plans to acquire Time

Warner Inc. for roughly $182 billion in stock and debt Monday,

creating a digital media powerhouse with the potential to reach

every American in one form or another.

With

dominating positions in the music, publishing, news, entertainment,

cable and Internet industries, the combined company, called AOL Time

Warner, will boast unrivaled assets among other media and online

companies.

The

merger, the largest deal in history, combines the nation’s top

internet service provider with the world’s top media conglomerate.

The deal also validates the Internet’s role as a leader in the new

world economy, while redefining what the next generation of

digital-based leaders will look like.

"Together, they represent an unprecedented

powerhouse,” said Scott Ehrens, a media analyst with Bear Stearns.

"If their mantra is content, this alliance is unbeatable. Now they

have this great platform they can cross-fertilize with content and

redistribute.”

Source:

CNN Money

Two years later the new accounting standards required the impairment

of goodwill which resulted in the largest write-down:

What AOL Time Warner's $54 Billion Loss Means

By Frank Pellegrini Thursday, Apr. 25, 2002

Sticking out of AOL Time Warner's rather

humdrum earnings report Wednesday was a very gaudy number: A

one-time loss of $54 billion. It's the largest spill of red ink,

dollar for dollar, in U.S. corporate history and nearly two-thirds

of the company's current stock-market value. (It's also, as a lot of

news outlets have noted, more than the annual GDP of Ecuador, but

that's hardly relevant here.) All for something called "goodwill

impairment."

Source Time Business

Liabilities

Current Liabilities

This is the set of obligations that will fall due within one year or

one operating cycle. This

provides the other side of the working capital or operating cycle.

The operating cycle is the time to purchase, manufacture or

provide the inventory or service, sell the product or service for

cash or on account.

Some major line items are:

Accounts Payable (Category:

Operating)

These items are short-term obligations arising from credit extended

to a firm’s suppliers.

The length of time extended by suppliers typically represents the

tradeoff between providing incentives for quick payments and

disincentives (penalty interest) for slow payment.

Notes Payable (Category:

Operating and Financing)

These are short term promissory notes issued to suppliers and

financial institutions.

For example, Notes Payable is not a big deal to an Apple who is

sitting on globules of cash.

However, notes payable is a big deal to a Coca-Cola who

recently completed acquisitions that resulted from a major strategy

shift.

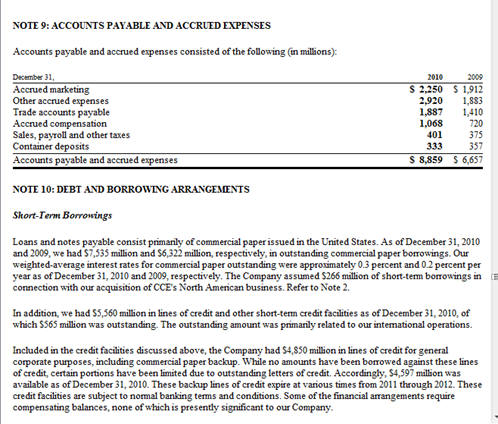

Example:

Again as an analyst you must consult the footnotes to the Balance

Sheet to get at the additional detail associated with specific

balance sheet line items:

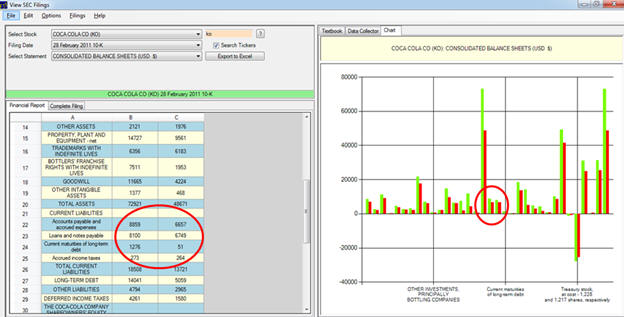

Current Maturities of Long-Term Debt (Category:

Financing)

These items are the long-term debt outstanding that falls due during

the current year. As a

result, it includes the face value of debt that matures during the

current year.

Accrued Liabilities (Category:

Operating)

This item results from accrual accounting.

These items arise from the recognition of expenses prior to

the actual cash being paid.

The credit part of the entry creates an accrued liability.

Unearned Revenue or Deferred Credits (Category:

Operating)

This item results from accrual accounting.

It arises when a firm is paid in advance for services or

product before delivery.

This is one of the most interesting areas of the balance

sheet for an analyst to review.

Why?

First this is a nice liability to have!

It is “unearned revenue” that has an obligation to deliver

services or products.

However, when delivered this becomes Sales Revenue.

Unearned revenue is typical in the technology sector because

a product can be a bundle of goods and services.

From an analyst perspective when forecasting next quarter’s

earnings and revenue large amounts of unearned revenue imply that a

firm may be more likely to meet consensus forecasts because it has

the additional flexibility of being able to convert its unearned

into earned revenue.

For example, a simple to understand “old economy” product such as

produced by Coca Cola result in no unearned revenue.

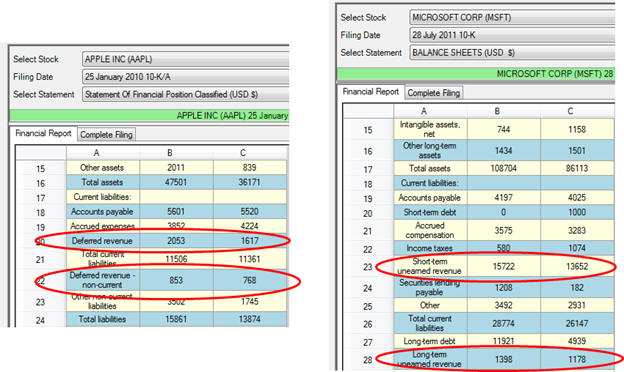

But for the case of technology stocks such as Apple,

Microsoft and Google unearned revenue may provide powerful signals

to analysts.

For the case of Microsoft and Apple these very strong deferred

revenue numbers provide each stock with a lot of flexibility for

meeting quarterly revenues.

The efforts required to generate the initial sale have

already been performed and to be recognized as accounting revenue

the remaining services or product must be delivered.

That is, it does not require generating future sales.

For both of these companies their subsequent 10-Q’s resulted in

strong announced results:

Microsoft News Center

News Press Release

Microsoft Reports Record Revenue of $20.9

Billion in Second Quarter

Strong business demand and holiday sales

drive record revenue and EPS.

REDMOND, Wash. — Jan. 19, 2012 — Microsoft

Corp. today announced quarterly revenue of $20.89 billion for the

quarter ended Dec. 31, 2011, a 5% increase from the prior year

period. Operating income, net income, and diluted earnings per share

for the quarter were $7.99 billion, $6.62 billion, and $0.78 per

share, compared with $8.17 billion, $6.63 billion and $0.77 per

share, respectively, in the prior year period. Prior year results

include recognition of $224 million of deferred revenue related to

the Office 2010 technology guarantee program.

Apple Press Information

Apple Reports First Quarter Results

Highest Quarterly Revenue and Earnings Ever

All-Time Record iPhone, iPad and Mac Sales

CUPERTINO, California—January 24, 2012—Apple® today announced

financial results for its fiscal 2012 first quarter which spanned 14

weeks and ended December 31, 2011. The Company posted record

quarterly revenue of $46.33 billion and record quarterly net profit

of $13.06 billion, or $13.87 per diluted share. These results

compare to revenue of $26.74 billion and net quarterly profit of $6

billion, or $6.43 per diluted share, in the year-ago quarter. Gross

margin was 44.7 percent compared to 38.5 percent in the year-ago

quarter. International sales accounted for 58 percent of the

quarter’s revenue.

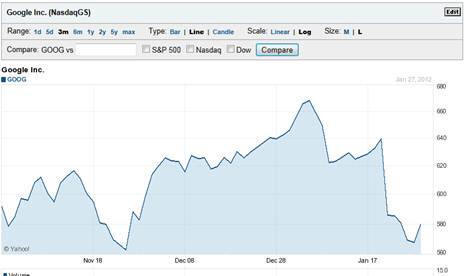

This can be contrasted to Google.

Their quarterly results were not so strong relative to

analyst forecasts:

Bloomberg

Google Quarterly Earnings Miss Hands 99%

Losses to Bullish Options Traders

By

Nikolaj Gammeltoft and Jeff Kearns - Jan 20, 2012 4:32 PM ET

Google Inc. (GOOG) options traders who made

bullish bets before the company’s quarterly report yesterday

suffered the U.S. derivatives market’s biggest losses today after

the search-engine operator missed analysts’ projections.

Google calls posted 10 of the 12 biggest

declines among all contracts traded on U.S. exchanges as of 4 p.m.

New York time, with each tumbling more than 99 percent, according to

data compiled by Bloomberg. Shares of the Mountain View, California-

based company tumbled 8.4 percent, the most since December 2008.

January $595 calls, which expire today, retreated 99.98 percent for

the biggest drop.

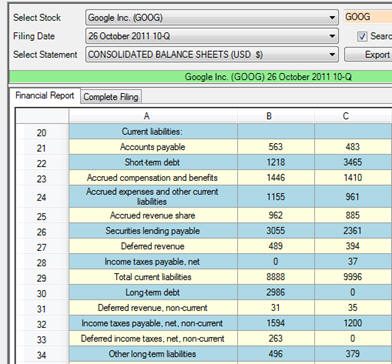

It is interesting to contrast Google’s unearned revenues for the

previous quarter.

Google’s deferred revenues are substantially lower than for an Apple

or a Microsoft and thus Google has less flexibility to meet analyst

expectations:

Missing the sell side analyst forecasts is costly not only to option

traders betting on Google but to the stock in general.

Deferred

Income Taxes (Category:

Operating)

This item results from temporary differences in the recognition of

revenue and expense for taxable income relative to reported income.

The item is governed by FAS 109 and it arises from

differences when calculating taxable and accounting income.

It is noted that no legal obligation exists for deferred

taxes but the items included in deferred taxes are only those items

which are judged to give rise to temporary differences between

taxable and accounting incomes.

Permanent differences are not included in Deferred Taxes.

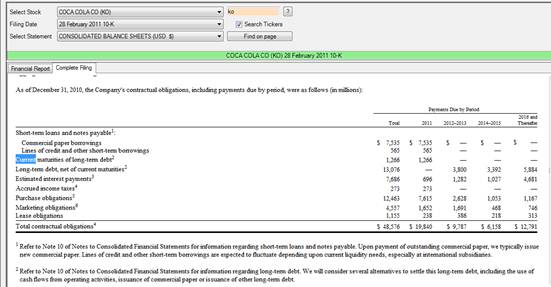

Long Term Debt (Category:

Financing)

These items are all financial obligations with maturities in excess

of one year. Long term

debt is the residual portion of long term debt that does not fall

due within the next year.

This latter debt is labeled:

Current Maturities of Long-Term Debt

The balance sheet numbers represent aggregate numbers and companies

are required to provide additional financing details in the

footnotes to the consolidated balance sheet (plus other places) as

illustrated for Coca-Cola below:

Capital Lease Obligations (Category:

Financing)

These items arise from the credit entry arising under both US GAAP

and IFRS when leases are recognized as an asset.

That is, if the firm bears substantially all the risks and

rewards of ownership of the leased property this is classified as a

capital lease and both an asset and liability are recorded on the

balance sheet. A lease

liability and lease asset is recognized if any one of four

conditions are met:

•

Lease transfers ownership, contains a “bargain” purchase option,

lease life >= 75% life of asset, lease payments have a PV of 90% or

more of the fair property value

Otherwise it is treated as an operating lease which has no balance

sheet liability implications.

However, US GAAP does require footnote disclosure of leases

and so an analyst can estimate what the Asset and Liability

implications would be if it was treated as a Capital Lease.

This is important if comparing three types of firms.

Firm A owns capacity, Firm B leases the same capacity

structured as an operating lease and Firm C leases the same capacity

structured as a capital lease.

Economically Firms A, B, and C all have the same capacity but

the accounting is very different for Firm B versus A and C.

For the case of B no capacity is recorded on the balance

sheet whereas capacity is recorded for A and B.

As a result, analysts by referring to the footnote

information reassess B’s operating lease as a capital lease to

ensure compatibility if the lease is significant.

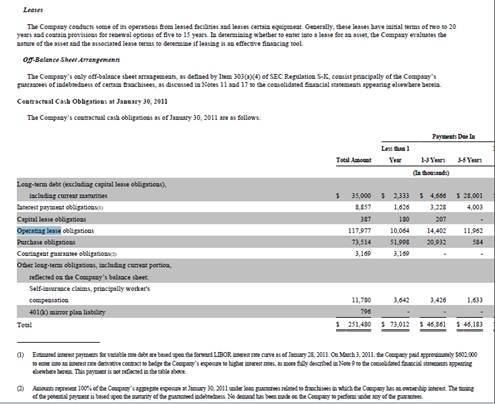

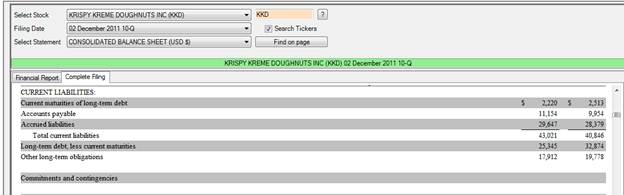

For example, Krispy Kreme current footnote disclosure is as follows

which classifies leases into Capital and Operating:

Postretirement Benefits Other Than Pensions (PRB) (Category:

Operating)

There are two general types of pensions, Defined Benefits and

Defined Contributions.

The latter is common today and has straightforward accounting

implications (Debit Pension Expense and Credit

Cash or Payables).

For the case of defined benefits things are not straightforward.

SFAS 158 (US GAAP) 2006 extended the reporting of defined

benefit plans to communicating the funded status of defined benefit

pension plans as opposed to a detailed pension footnotes.

That is, under SFAS 158,

company “defined benefit” pension plans must recognize the

difference between the projected $ benefit obligation and the fair

value of the plan’s assets as either an asset or a liability.

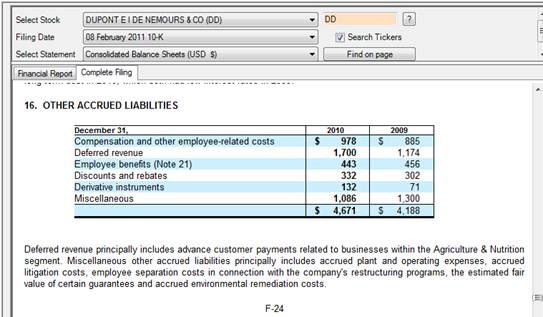

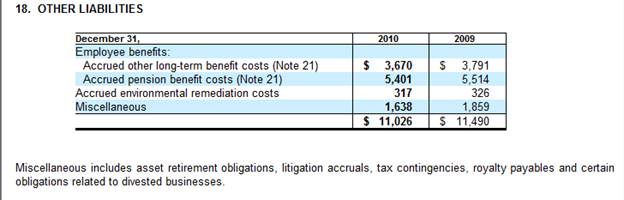

Old economy companies can have significant defined benefit

obligations. For

example, DuPont the oldest company in the Dow Jones 30 stocks

reports as follows as “Other Accrued Liabilities:

And further as “Other Liabilities”:

That is, significant defined benefit obligations exist that are

lumped into the above “Other” categories on the Balance Sheet.

It is interesting to observe as a side note that DuPont also

include their Deferred Revenues in Other Accrued Liabilities.

Commitments and Contingencies (Category:

Operating)

This line item can appear on a balance sheet without an amount

beside. It is itemized

to direct a reader’s attention to the disclosures included in the

notes to the financial statements.

Items include non-cancellable leases or other non-cancellable

contracts which are disclosed even if no amount is due at the time

of the Balance Sheet.

For example, consider the following for Krispy Kreme

Commitments and contingencies is listed with a blank beside it.

However, in the footnote information the following additional

information is disclosed:

Note 5 — Commitments and Contingencies

Except as disclosed below, the Company currently is not a party

to any material legal proceedings.

Pending Litigation

On April 7, 2009, a Cayman Islands corporation, K2

Asia Ventures, and its owners filed a lawsuit in Forsyth County,

North Carolina Superior Court against the Company, its

franchisee in the Philippines, and other persons associated with

the franchisee. The suit alleges that the Company and the other

defendants conspired to deprive the plaintiffs of claimed

“exclusive rights” to negotiate franchise and development

agreements with prospective franchisees in the Philippines, and

seeks unspecified damages. The Company believes that these

allegations are false and intends to vigorously defend against

the lawsuit.

Other Legal Matters

Other Commitments and Contingencies

The Company has guaranteed certain loans from third-party

financial institutions on behalf of Equity Method Franchisees

primarily to assist the franchisees in obtaining third-party

financing. The loans are collateralized by certain assets of the

franchisee, generally the Krispy Kreme store and related

equipment. The Company’s contingent liabilities related to these

guarantees totaled approximately $2.7 million at October 30,

2011, and are summarized in Note 8. These guarantees require

payment from the Company in the event of default on payment by

the respective debtor and, if the debtor defaults, the Company

may be required to pay amounts outstanding under the related

agreements in addition to the principal amount guaranteed,

including accrued interest and related fees.

The aggregate recorded liability for these loan guarantees

totaled $1.9 million as of October 30, 2011, which is included

in accrued liabilities in the accompanying consolidated balance

sheet. These liabilities represent the estimated amount of

guarantee payments which the Company believed to be probable.

While there is no current demand on the Company to perform under

any of the guarantees, there can be no assurance that the

Company will not be required to perform and, if circumstances

change from those prevailing at October 30, 2011, additional

guarantee payments or provisions for guarantee payments could be

required with respect to any of the guarantees.

In addition, accrued liabilities at October 30, 2011, includes

approximately $990,000 related to the Company’s assignment of

operating leases on refranchised stores. The Company is

contingently liable to pay the rents on these stores to the

landlords in the event the assignees fail to perform under the

leases they have assumed. During the second quarter of fiscal

2012, the Company recorded a provision of $820,000 for payments

the Company expects to make under a lease guarantee related to a

franchisee whose franchise rights the Company terminated during

the second quarter. During the third quarter of fiscal 2012, the

Company reversed a previously recorded lease guarantee accrual

of $110,000 as a result of the Company receiving a release from

the related guarantee. The aggregate gross guarantee exposure

under all such lease guarantees, without reduction for any

potential sublease rentals or any other mitigation, was

approximately $4.2 million as of October 30, 2011.

One of the Company’s lenders had issued letters of credit on

behalf of the Company totaling $10.2 million at October 30,

2011, all of which secure the Company’s reimbursement

obligations to insurers under the Company’s self-insurance

arrangements.

In addition to entering into forward purchase contracts, the

Company from time to time purchases exchange-traded commodity

futures contracts or options on such contracts for raw materials

which are ingredients of the Company’s products or which are

components of such ingredients, including wheat and soybean oil.

The Company typically assigns the futures contract to a supplier

in connection with entering into a forward purchase contract for

the related ingredient. The Company may also purchase futures,

options on futures or enter into other hedging contracts to

hedge its exposure to rising gasoline prices. See Note 11 for

additional information about these derivatives.

The Company also is engaged in various legal proceedings arising in

the normal course of business. The Company maintains customary

insurance policies against certain kinds of such claims and suits,

including insurance policies for workers’ compensation and personal

injury, some of which provide for relatively large deductible

amounts.

Non-Controlling Interests (Category:

Financing)

This arises when the parent controls less than 100% of the

subsidiary and it gives rise to a line item now described as

“Non-controlling Interest.”

This represents a name change from the traditional label

“Minority Interest” resulting from FAS 160 to emphasize a parent’s

substantive control over a subsidiary rather than a simple ownership

percentage to better reflect the underlying economic and accounting

concepts.

Finally we present a summary of Stockholders’ Equity accounts below

but return to these items in more detail in the section on the

Consolidated Statement of Stockholders’ Equity.”

Stockholders’ Equity

The residual ownership rights in the company are presented in the

this last section of the Balance sheet.

This represents the residual claims against the Assets net of

Liabilities. These

residual owners bear the risks and rewards of from the firm.

Common Stock (Category:

Financing)

The amount listed here is based upon the par or partly paid value of

the shares issued. This

usually bears no relationship to the market value of the stock as it

is based upon the legal par value.

Additional Paid-In Capital (Category:

Financing)

The amount listed here measures the amount by which the original

sales price of the shares exceeded the par amount.

Retained Earnings (Category:

Operating)

This account contains the record of cumulative earnings from the

firm since its inception net of dividends paid.

Accumulated Other Comprehensive Income (Category:

Operating)

This amount comes from the Statement of Stockholders’ Equity.

It largely includes the results from four items:

Unrealized gains and losses in the market value of investments

for-sale securities.

Excess of additional pension liability over unrecognized prior

service cost

Gains and losses from derivatives

Foreign currency translations

Other Equity Accounts (Category:

Financing)

This can contain preferred stockholder claims which are usually paid

a fixed dividend relative to some face or par amount.