7.25

Appendix A:

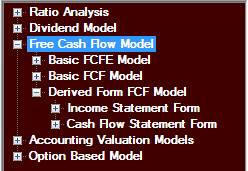

Variations to the FCFE Model Covered by Valuation Tutor

There is a wide variety of choices depending upon what source data

you want to work with plus what finer points you want to deal with.

The model variations are as follows:

i.

Basic FCFE Model

ii.

Basic FCFF Model

iii.

Derived Form FCFF Model

In addition, for the basic FCFE and

FCFF models the software provides you with the choice of applying

this as a 1- or 2-stage growth model.

For the case of the 1-stage model this is equivalent to

constant growth model discussed in the previous chapter using

estimated economic dividends as opposed to using the firm’s actual

dividend policy. For

the case of the 2-stage model this allows for economy wide

constraints to be formally incorporated into the analysis as well as

allowing the firm to experience some finite period of time where

growth rates may exceed economy wide constraints.

In this appendix we will focus on the differences in the models from

the perspective of the inputs holding the growth behavior issues

aside. The chapter

worked through both the basic FCFE and FCFF forms of the model.

We highlight the differences in the Valuation Tutor

calculator as follows:

Model ii:

FCFE versus FCFF Form Calculators

The tree diagram of possibilities is as follows:

First we will work directly both the FCFE and the FCFF models under

the simplifying assumption that the firm has some target debt ratio.

When this assumption is imposed the only difference between

the two calculators is:

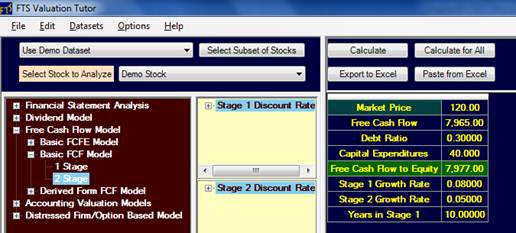

Free Cash Flow to Equity

(FCFE) = Free Cash Flow (FCFF) + Capital Expenditures * (Debt Ratio)

This is depicted below:

FCFF: Calculator

You can see by comparing the two calculators they are the same apart

from FCFE starts directly with FCFE whereas the second calculator

starts directly with FCFF, Capital Expenditure and the target debt

ratio. It then computes

FCFE from:

Free Cash Flow to Equity (FCFE) = Free Cash Flow (FCFF) + Capital Expenditures * (Debt Ratio)

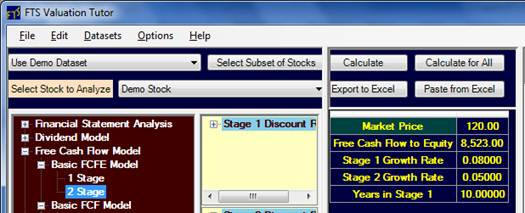

In relation to the second calculator the detailed inputs derived for

IBM in this chapter were:

Current Summary on

a Per Share Basis:

IBM Adjusted Cash Flows from Operations = 18.873/1.341 = 14.07

CAPEX per Share = 6.519/1.341 = 4.86

Derived Value: FCFF per share = 12.381/1.341 = 9.21

Debt Ratio = 0.239

Derived Value: FCFE per share = 13.939/1.341 = $10.39

5-year Stage 1 Growth:

0.10

Normal Growth:

0.045

Risk free rate (both stages) = 0.0419

Beta IBM = 0.76

Years in Stage 1:

5-years

Equity Premium = 0.055

Derived Value (CAPM):

Cost of Equity Capital = 0.0837

The different models available in the Valuation Tutor start from

different places in the analysis.

Model ii: appears as

follows:

Observe that the inputs for this model start from Free Cash Flow,

CAPEX and the Debt Ratio inputs with all others being the same as

before:.

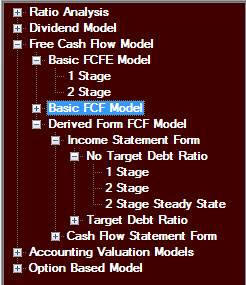

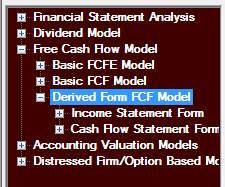

Derived Forms of the

FCFF Model

In section I. of this chapter some variations for computing the FCFF

were presented using Cash Flow from Operations and then Accounting

Net Income and so on.

So now refer back to the Valuation Tutor screen and click on Derived

Form FCFF Model as follows:

Here there are two basic formats supported by the calculator.

First, is the Income Statement Form and the second is the

Cash Flow Statement Form.

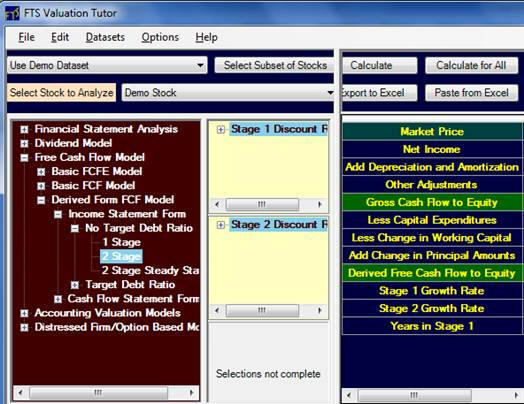

Consider the Income Statement Form of the model first with no

simplifying Target Debt Ratio assumption imposed.

Selecting this combination as depicted below the screen will

now appear as follows:

Recall from section I we defined FCFF from Net Income as:

Accounting Income Form of FCFF

Free Cash Flow (FCFF) = Net Income (NI) + Non-Cash Expenses (NCE)

+Interest Expense (Int) Net of Tax(tc)

– Investment in Capacity (InvCapacity) –

Investment in Working Capital (InvWC)

FCFF = NI + NCE + Int*(1-tc) – InvCapacity -

INVWC

And further to get to FCFE this is:

FCFE = FCFF – Interest*(1 – Tax Rate) + Net Borrowing

FCFE = NI + NCE + Int(1-tc) -

So from the above the inputs are:

Accounting NI

Non Cash Expenses

Interest expense net of tax

Investment in Capacity

Investment in Working Capital