6.13 IBM Example

Our

historical analysis of IBM suggested a growth rate of dividends of

8. This is higher than

the economy’s growth rate, and was greater than the discount rate,

so we could not use this in the one stage model. Let’s see how the

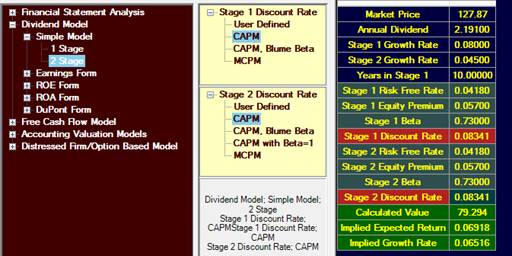

two stage model values IBM if the first stage growth rate is 8% and

the remaining parameters are as shown on the screen:

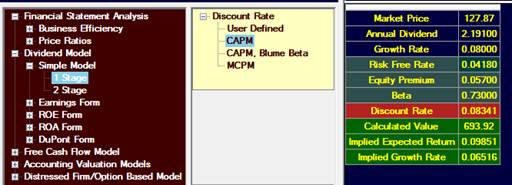

Compare this to

the one-stage model with the same parameters:

You can see

impact of limiting the second stage growth rate on the valuation.

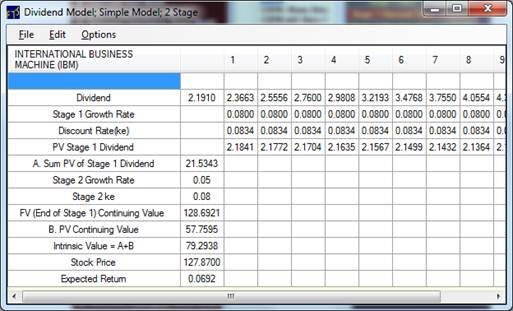

When you

calculate the two stage model, Valuation Tutor provides you with the

details of the calculation:

This shows you

exactly how the values are calculated, and serves as a reference

point for understanding the details.

You can export this into Excel and see if you can verify the

steps of the calculation.

Projecting Future Prices

As we noted

before, Valuation Tutor also reports the implied expected return.

One way to use that number is to project future prices.

For example, if the current price is $100 and the expected

return from the valuation model is 10%, then you have a projected

price, or a price target of $110 in one year.

Criticism of Model 2

The two stage

model is a clear improvement over the one stage model particularly

because it lets us restrict long term growth in an economically

meaningful manner.

But three major

limitations remain:

i.

The model only applies to stocks that pay dividends and have a

stable dividend policy.

But many companies have a more complex dividend policy that consists

of both accounting dividends and Treasury stock purchases.

These purchases create important changes to shareholders

equity that are not accounted for in the dividend model

ii.

Implicit in the model is the assumption that the firm is a going

concern. Some firms may

be distressed, and the model will not be useful for these companies.

iii.

The model is clearly not applicable to a non-dividend paying stock.

In the next

chapters, we introduce extensions of the dividend model that can

overcome some of these limitations.

These are the free cash flow to equity model, residual

income model and the abnormal earnings growth model.

In Chapter 8, we study a model specifically applicable to

distressed stocks.