6.10 Example:

IBM’s Cost of Equity Capital from CAPM

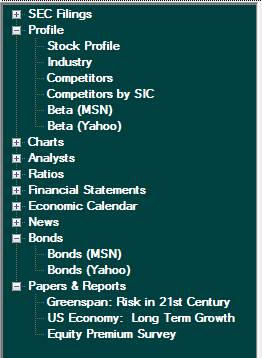

Valuation Tutor’s information system provides quick access to

information to apply the CAPM:

Under “Bonds,” you can find rates on US Treasuries.

You may want to pick a long term interest rate, since we

are going to be discounting the dividends for a long time (in

fact, forever!).

At the time of this writing, the yield on the 30 year

Treasury bond was 4.18%.

To get an estimate of beta, select one of the sources under

“Profile.” At the time

of this example, IBM’s beta was 0.73.

Now we need the equity premium.

Many sources report an equity premium, and the estimates

can vary quite a bit.

Under “Papers and Reports,” we have a link to a paper by

Professors Pablo

Fernandez and Javier Del Campo Baonza at the University of

Navarra, who did an extensive survey of estimates of the equity

premium. The consensus estimates are in the 5.1% to 5.3%, and

most estimates fell between 5.1% and 5.5%. We will use 5.1% in

our examples.

Our estimated inputs provide you with an estimate of ke

for IBM:

Note:

the CAPM only provides the discount rate for cash flows (like

dividends) that accrue to shareholders.

It does not provide a discount rate for the cash flows of

the firm as a whole (so payments that accrue to both

shareholders and bond holders).

For a firm as a whole, the discount rate is usually

specified as a weighted average of ke and the yield

on the debt of the firm, kd.

The WACC, or weighted average cost of capital, is defined

by:

Here, τc is the corporate tax rate.

The equation works with the after tax cost of debt

because interest expense is tax deductible while dividend

payments are not.